Potash Market Dynamics: Balancing Food Security and Geopolitics

Potash is becoming an increasingly strategic commodity as food security concerns, concentrated global supply and geopolitical risk reshape the market.

Why does potash remain one of the world's least financialised commodities?

What does its growing importance mean for producers, traders and policymakers?

Enco Insights, London - 06 July 2026

Potash, a potassium-rich mineral used mainly to make fertilisers that help crops grow, is moving up the strategic agenda. Food security, concentrated supply, and new capacity are reshaping how the market is viewed.

Food Security and Supply Concentration

Macro trends, including population growth and rising incomes, continue to support demand for the three main fertiliser nutrients: nitrogen (N), phosphate (P), and potash (K), collectively known as NPK:

Nitrogen (N) drives leaf and plant growth.

Phosphate (P) supports root development and energy transfer in plants.

Potash (K) supplies potassium, improving plant health, water-use efficiency and crop yield.

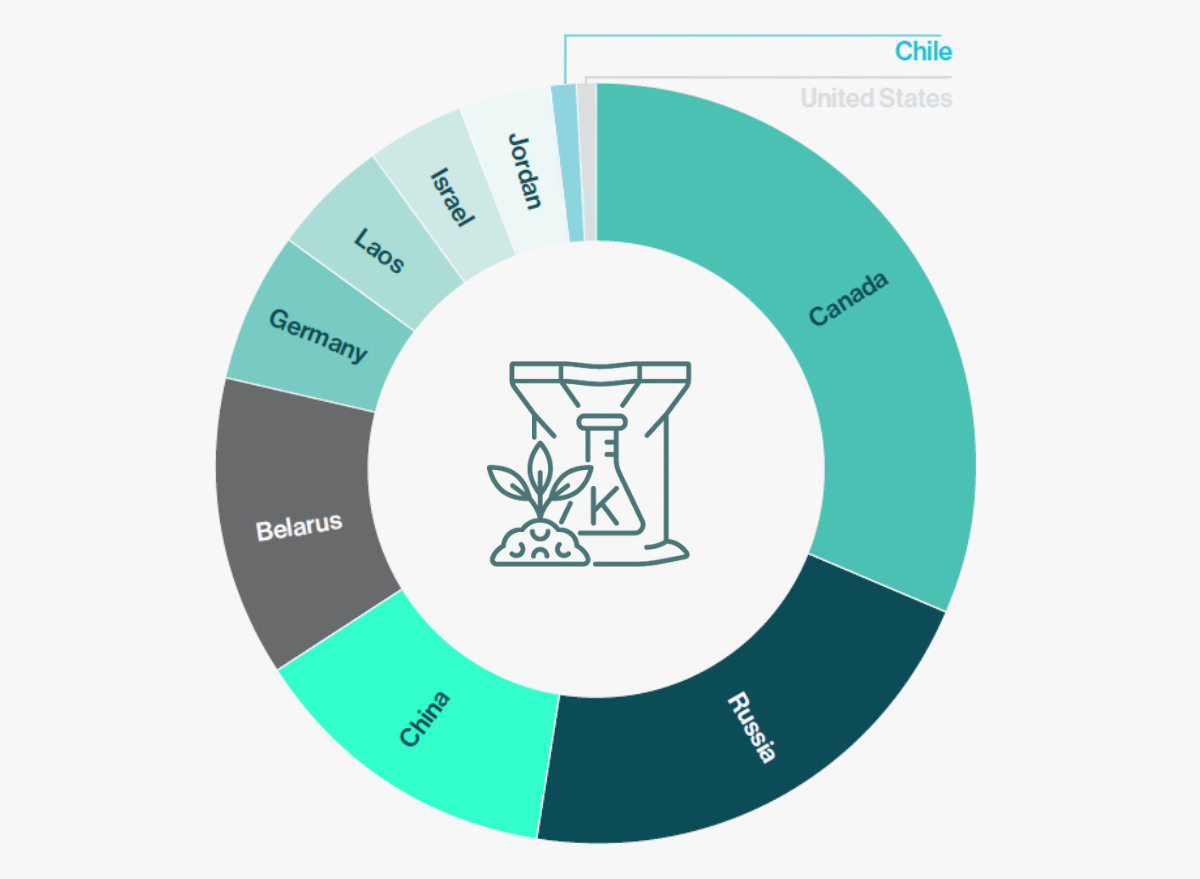

Production remains highly concentrated: Canada, Russia, China and Belarus account for approximately 76% of global production, according to the USGS Mineral Commodity Summaries published in February 2026.

New supply options exist, but the route from deposit to production remains difficult. Although new deposits are being explored in jurisdictions including Morocco, Ethiopia, and West Africa, bringing new capacity to market remains challenging. Morocco's Khemisset dispute, now before the International Centre for Settlement of Investment Disputes (ICSID), illustrates how permitting, water use, and political risk can delay otherwise attractive projects.

Why Potash Markets Operate Differently

Potash also remains less financialised and more structurally controlled than other major commodity markets.

It sits at the intersection of food security and geopolitics but operates differently from most commodities. The distribution of potash is largely direct to end users, limiting the role of intermediaries and shaping how the market functions.

The inclusion of potash on the US Critical Minerals list in 2025 reflects its growing strategic importance, particularly as supply remains concentrated in the regions mentioned above.

Potash has over-the-counter (OTC) activity and Price Reporting Agency (PRA) coverage, but it lacks a deep, liquid, exchange-cleared futures or swaps market of meaningful scale.

Price discovery remains anchored in physical contracts, major China and India import settlements, tenders, and regional PRA assessments. A sizeable derivatives market appears unlikely to emerge in the near term, reflecting a market structure that limits arbitrage opportunities.

Global potash production by country 2025

A Tale of Two Markets

This contrasts with nitrogen markets, which are more cyclical, more closely linked to energy prices, and more actively traded by intermediaries. Nitrogen application is relatively difficult for farmers to defer without affecting yields.

Potash demand is different. Farmers can defer application for a period by drawing on existing soil reserves, particularly when prices are high. Precision agriculture reinforces this distinction: for nitrogen, it shapes annual application decisions, while for potash, it can support reduced or delayed applications where soil potassium levels are sufficient.

Nitrogen’s exposure to gas prices, active trade flows, and shorter-term demand response has helped create a more liquid and intermediary-led market. Potash, by contrast, remains more dependent on producer relationships, bilateral contracts and periodic benchmark settlements. Its limited financialisation reflects the industry’s underlying structure.

Eden heads up business development at our advisory practice. He previously built the market intelligence and investor relations functions at Swedish battery startup Cling Systems. At Cling, he also contributed significantly to origination, focusing on energy storage companies, recyclers, OEMs, traders, and financiers. Prior to Cling, he spent nine years at Brunswick Group in London and Stockholm, advising FTSE 100 companies, startups, and scale-ups.

“Potash is moving beyond its traditional role as a fertiliser input to become a strategic commodity shaped by food security, geopolitics and supply concentration.”

From Fertiliser to Critical Mineral

The policy treatment of potash reinforces the same point. Its inclusion on the US Critical Minerals list last year reflects concerns over import reliance, food security and concentrated global supply. The US Geological Survey notes that the US remains highly import-dependent for potash, with Canada accounting for 79% of US import sources over 2021–24.

Enco Insights is a dedicated advisory network for the energy, infrastructure, and resources

sectors. We leverage a global network of industry advisors and operating executives across energy, infrastructure, and resources.

We have built deep, high-trust relationships with a carefully curated group of practitioners, enabling us to connect clients quickly with the most relevant expertise for each situation.